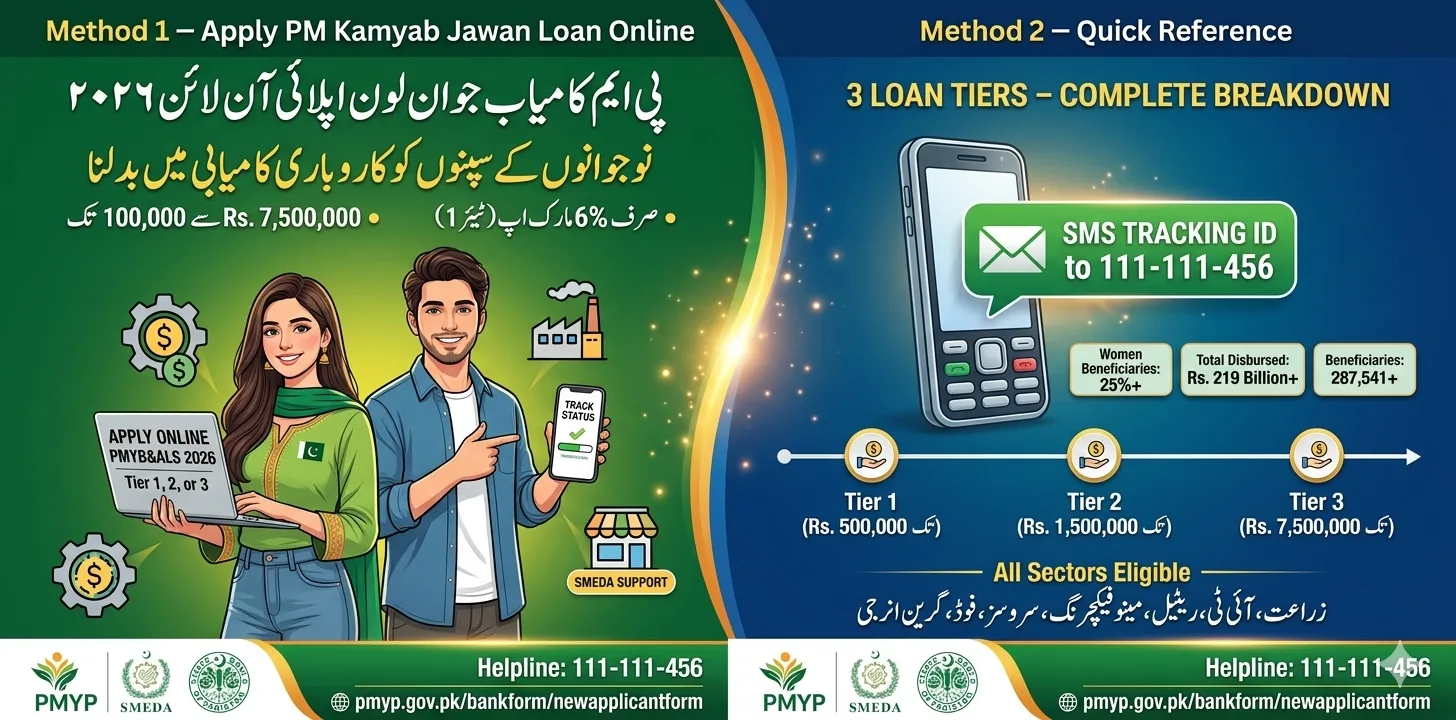

The PM Kamyab Jawan Loan 2026 , now officially known as the PM Youth Business & Agriculture Loan Scheme (PMYB&ALS) , is Pakistan’s flagship youth entrepreneurship initiative, providing subsidized loans from Rs. 100,000 to Rs. 7,500,000 through 15 partner banks to young Pakistanis aged 21–45 who want to start or grow a business.

Since its original launch as Kamyab Jawan in 2019 and its transformation into PMYB&ALS in December 2022, the scheme has disbursed over Rs. 219 billion to 287,541+ beneficiaries , turning thousands of young dreamers into successful business owners across agriculture, IT, retail, manufacturing, and services. With a 25% quota reserved for women, Tier 1 loans at just 6% markup (and 0% for microloans), and an entirely online application at pmyp.gov.pk, there has never been a better time for a young Pakistani to take this life-changing step.

Kamyab Jawan / PMYB&ALS 2026 – Quick Reference

| Detail | Information |

| Original Name | PM Kamyab Jawan Youth Entrepreneurship Scheme (PMKJ-YES) |

| Current Official Name | PM Youth Business & Agriculture Loan Scheme (PMYB&ALS) |

| Renamed By | PM Shehbaz Sharif government , December 2022 |

| Official Portal | pmybals.pmyp.gov.pk |

| Apply Online | pmyp.gov.pk/bankform/newapplicantform |

| PMYP App | Digital Youth Hub (Android & iOS) |

| Loan Range | Rs. 100,000 – Rs. 7,500,000 |

| Tier 1 Markup | 6% per annum (govt subsidizes difference) |

| Tier 1 Microloan | 0% (Interest-Free) for micro category |

| Women’s Quota | 25% strictly reserved |

| Partner Banks | 15 Commercial, Islamic & SME Banks |

| Total Disbursed | Rs. 219 Billion+ to 287,541+ youth |

| SMEDA Helpline | 111-111-456 (Free advisory, all provinces) |

| SBP Regulated | Yes , under SBP Circular IH&SMEFD |

From Kamyab Jawan to PMYB&ALS – The Full Story

Understanding this evolution is critical , and most competitors get it wrong.

The Prime Minister’s Youth Programme was renamed to the Kamyab Jawan Program by the Imran Khan ministry in September 2019, and after a pause in disbursements from July 2022, was renamed back by the Shehbaz Sharif ministry in December 2022.

The current scheme , PMYB&ALS , is not a replacement but an upgraded, expanded version of Kamyab Jawan:

| Feature | Original Kamyab Jawan (2019–2022) | PMYB&ALS 2026 (Current) |

| Max Loan | Rs. 5,000,000 | Rs. 7,500,000 |

| Agriculture Focus | Limited | Fully integrated , all crop/non-crop sectors |

| Microloans (0%) | Not included | Added , interest-free microloan tier |

| Application | Partial online | 100% online , no physical form |

| Women’s Quota | 25% (informal) | 25% strictly enforced |

| Partner Banks | Initially 3 (NBP, BOP, Bank of Khyber) | 15 Commercial, Islamic & SME banks |

| Islamic Banking | Not formalized | Shariah-compliant modes available |

| IT Age Limit | 18+ | 18+ with Matric minimum |

| Status | Paused July 2022 | Active , Apply Now |

The Government of Pakistan approved revisions in the key features of PMKJ-YES to make it more purposeful and beneficial for small businesses and agriculture. The new components of interest-free microloans and agriculture loans have been added to the scheme.

3 Loan Tiers – Complete Breakdown

PMYB&ALS divides loans into three tiers to suit different business scales. Equity requirements apply to new businesses (10% for T1/T2, 20% for T3), while existing businesses need none.

| Feature | Tier 1 | Tier 2 | Tier 3 |

| Loan Amount | Rs. 100,000 – Rs. 500,000 | Rs. 500,000 – Rs. 1,500,000 | Rs. 1,500,000 – Rs. 7,500,000 |

| Markup Rate (Borrower) | 6% p.a. | 8% p.a. | Market rate (subsidized) |

| Repayment Period | Up to 3 years | Up to 5 years | Up to 8 years |

| Grace Period | Mutually agreed (optional) | Up to 1 year | Up to 1 year |

| New Business Equity | 10% | 10% | 20% |

| Existing Business Equity | Nil (Zero) | Nil (Zero) | Nil (Zero) |

| Collateral | Usually None | Vehicle as collateral | Vehicle/asset required |

| Civil Works Financing | Up to 65% | Up to 65% | Up to 65% |

| Best For | Micro-entrepreneurs, first-timers | Growing SMEs, skilled trades | Manufacturers, IT firms, large farms |

Hidden gem from HBL official: A customer may avail two loans (one short term and one long term) simultaneously within the overall financing limit of PKR 7.5 million. Thus, two loans may be availed at the same time. Most people don’t know this , you can run a working capital AND a long-term loan concurrently under PMYB&ALS.

Who Is Eligible – 2026 Criteria

All citizens of Pakistan holding CNIC, aged between 21 and 45 years with entrepreneurial potential are eligible. For IT/E-Commerce related businesses, the lower age limit will be 18 years and at least matriculation or equivalent education will be required. The above age condition is applicable on individuals and sole proprietors. In case of all other forms of business including partnerships and limited companies, only one of the owners, partners or directors must be in the age bracket prescribed above.

Full Eligibility Checklist:

- ✅ Pakistani resident , scheme is for resident Pakistanis only

- ✅ Age 21–45 years (general) | 18–45 years for IT/e-commerce

- ✅ Valid CNIC or SNIC

- ✅ Clean e-CIB record , no bank defaults

- ✅ Not a government employee at any level

- ✅ Not enrolled in another federal/provincial loan scheme

- ✅ Viable business plan , all sectors qualify

- ✅ Women entrepreneurs: 25% quota reserved , priority processing

Blood relatives of employees of a participating bank cannot apply for loans under this scheme from the bank where their blood relatives are employed. An important rule most guides miss , choose a bank where no immediate family member works.

Documents Required – Complete 2026 Checklist

| Document | Required For | Details |

| CNIC / SNIC (Front & Back) | All Tiers | Valid, not expired |

| Passport-Size Photo (2) | All Tiers | Recent, clear |

| Business Feasibility Report | All Tiers | 1–2 pages: idea, revenue projection, costs |

| Proof of Residence | All Tiers | Utility bill or rent agreement |

| NTN (National Tax Number) | Tier 2 & 3 | Free registration at FBR.gov.pk |

| Bank Statement (6 months) | Tier 2 & 3 | Demonstrates financial activity |

| Educational Certificate | IT/e-commerce (18+) | Matric minimum for IT applicants |

| References (2 non-relatives) | Tier 2 & 3 | CNICs and contact numbers |

| Vehicle Registration | If vehicle = collateral | T2/T3 as security |

2026 portal update: Please ensure to fill in the required fields of Applicant’s CNIC Number, CNIC Issue date and DOB correctly as they will be verified by NADRA. Please read the form carefully before applying. Submitted form cannot be changed hence the wrong information can affect the approval of your application.

How to Apply Online – Step-by-Step 2026 Guide

No physical application form is required. All applications have to be submitted online at the following address: https://pmyp.gov.pk/bankform/newapplicantform

Complete Application Process:

- Visit → pmyp.gov.pk/bankform/newapplicantform

- Register using CNIC, mobile number, and email address

- Verify OTP sent to your registered SIM

- Select your loan tier (Tier 1, 2, or 3)

- Choose your partner bank from the dropdown , select based on your nearest branch

- Fill personal, educational, and business details , name, address, sector, expected turnover

- Upload all documents in clear JPG or PDF format

- Submit the application , note your Tracking ID

- Track status at pmybals.pmyp.gov.pk or SMS Tracking ID to helpline

- Bank contacts you , keep mobile ON; bank will call for verification

One applicant can upload a maximum of two applications against his/her CNIC/SNIC. If your first application is with one bank, you can submit a second to another bank , maximizing approval chances.

Sectors Eligible for Kamyab Jawan / PMYB&ALS 2026

All sectors and products are eligible. Moreover, in the case of agriculture, all crop and non-crop sectors (including crop production, livestock, poultry, fishery, dairy etc.) are also eligible.

| Sector | Examples | Special Notes |

| Retail & Trade | Shops, wholesale, import-export | All scales , from street vendor to distributor |

| Agriculture | Crops, livestock, poultry, fishery, dairy | All crop and non-crop sectors confirmed |

| IT & E-Commerce | Freelancing, apps, SaaS, online stores | Age limit 18+; Matric required |

| Manufacturing | Garments, food processing, small factories | Up to 65% civil works financing |

| Services | Salons, academies, repair shops, clinics | Tier 1 ideal for service startups |

| Green Energy | Solar businesses, clean tech | Prioritized in 2026 processing |

| Food & Hospitality | Restaurants, bakeries, food carts | Vehicle financing available (1 per customer) |

| Islamic / Sharia Compliant | Any sector via Meezan Bank, Bank Alfalah Islamic | Financing through Shariah-compliant modes: Musawamah, Istisna, and Diminishing Musharakah (DM) |

15 Partner Banks – Choose the Right One

Loans provided under PMYB&ALS are processed through 15 Commercial, Islamic and SME banks.

| Bank | Type | Contact / Email |

| HBL (Habib Bank) | Commercial | hbl.com/business/sme |

| Bank Alfalah | Commercial | bankalfalah.com |

| UBL (United Bank) | Commercial | ubl.com.pk |

| Bank of Punjab (BOP) | Provincial | bop.com.pk |

| Sindh Bank | Provincial SME | pmloans@sindhbank.com.pk | 111-772-772 |

| Bank Al Habib | Commercial | bankalhabib.com |

| Meezan Bank | Islamic | meezanbank.com |

| Allied Bank (ABL) | Commercial | abl.com |

| Bank Alfalah Islamic | Islamic | bankalfalah.com/islamic |

| National Bank (NBP) | State-owned | nbp.com.pk |

| NRSP Microfinance | MFI , rural focus | nrsp.org.pk |

| Akhuwat (Islamic MFI) | Islamic MFI | akhuwat.org.pk |

How to choose your bank:

- ✅ Select the bank where you already have an account , smoother verification

- ✅ Choose based on branch accessibility , you will need to visit for signing

- ✅ For Islamic financing, select Meezan Bank or Bank Alfalah Islamic

- ✅ For rural/farming areas, NRSP Microfinance has the widest rural reach

- ❌ Do not select a bank where an immediate blood relative is employed

Real Success Stories – How PMYB&ALS Changed Lives

Over PKR 8.5 billion was disbursed to establish over 10,000 businesses in key sectors such as agriculture, manufacturing, and services. There were early success stories, such as female entrepreneurs scaling dairy businesses and trans-entrepreneurs entering the fashion industry.

Here are the types of businesses young Pakistanis are building with this loan in 2026:

| Business Type | Loan Used | Monthly Revenue (Typical) | Tier Used |

| Poultry farm (500 birds) | Rs. 400,000 | Rs. 80,000–120,000 | Tier 1 |

| Women’s stitching unit (5 machines) | Rs. 250,000 | Rs. 60,000–90,000 | Tier 1 |

| IT/freelancing setup | Rs. 150,000 | Rs. 100,000–200,000+ | Tier 1 |

| Grocery superstore | Rs. 1,200,000 | Rs. 150,000–250,000 | Tier 2 |

| Small restaurant / dhaba | Rs. 800,000 | Rs. 120,000–200,000 | Tier 2 |

| Dairy farm (20 cows) | Rs. 3,000,000 | Rs. 300,000–500,000 | Tier 3 |

| Garment manufacturing unit | Rs. 5,000,000 | Rs. 500,000–800,000 | Tier 3 |

Why Young Pakistanis Choose PMYB&ALS Over Conventional Loans

| Factor | PMYB&ALS | Commercial Bank Loan |

| Markup Rate | 6%–8% (govt subsidizes difference to KIBOR+500bps) | 20%–25% annual |

| Collateral | None for Tier 1 | Mandatory (property/gold) |

| For Youth Specifically | Yes , age bracket 21–45 | No age targeting |

| Women’s Quota | 25% reserved | No reservation |

| Application | 100% online | In-branch paperwork |

| Agriculture Inclusion | All crop/non-crop sectors | Selective, difficult terms |

| Government Credit Guarantee | Yes , SBP circular backing | No |

| Small Amounts | From Rs. 100,000 | Minimum Rs. 500,000–1,000,000 |

Free SMEDA Business Plan Support – 4-Province Guide

The biggest reason applications get rejected is a weak or missing business feasibility report. Regional SMEDA Helpdesks provide free advisory for PMYB&ALS applicants:

| Province | Address | Helpline |

| Punjab (Lahore) | 4th Floor, Aiwan-e-Iqbal Complex, Egerton Road | 042-111-111-456 |

| Sindh (Karachi) | 5th Floor, Bahria Complex II, M.T. Khan Road | 021-111-111-456 |

| KPK (Peshawar) | Ground Floor, State Life Building, The Mall | 091-111-111-456 |

| Balochistan (Quetta) | Bungalow 15-A, Chaman Housing Scheme, Airport Road | 081-2831623 |

SMEDA provides free business feasibility templates customized for every sector , retail, dairy, IT, poultry, garments, and more. Visit any helpdesk or call before starting your application.

2026 Scheme Statistics – Current Numbers

| Metric | Figure |

| Total Applications Received | 3,371,000+ |

| Approved Applications | 293,000+ |

| Loans Disbursed | 287,541 beneficiaries |

| Total Amount Distributed | Rs. 219 Billion+ |

| Rejection Rate | ~57% (mostly: e-CIB default, incomplete documents) |

| Women Beneficiaries | 25%+ of total disbursements |

| Top Sector | Agriculture + IT combined |

Top 3 reasons for rejection (avoid these):

- e-CIB default record , check your credit history at any ECIB-reporting bank before applying

- Blurry or incomplete document uploads , scan in good light, check clarity before uploading

- CNIC data mismatch with NADRA , verify your CNIC details match exactly before submitting

Frequently Asked Questions (FAQs)

Q: What is the PM Kamyab Jawan Loan Scheme 2026? The PM Kamyab Jawan loan is now officially called the PM Youth Business & Agriculture Loan Scheme (PMYB&ALS). It offers subsidized loans of Rs. 100,000 to Rs. 7,500,000 to Pakistani youth aged 21–45 through 15 partner banks, with Tier 1 markup at 6% and interest-free microloans also available.

Q: Is the Kamyab Jawan loan still active in 2026? Yes. The scheme was paused briefly in July 2022, renamed PMYB&ALS in December 2022, and is fully active in 2026. Over Rs. 219 billion has been disbursed to 287,541 beneficiaries , apply at pmyp.gov.pk/bankform/newapplicantform.

Q: What is the difference between Kamyab Jawan and PMYB&ALS? They are the same scheme at their core , PMYB&ALS is the upgraded, renamed version launched under PM Shehbaz Sharif in December 2022. Key upgrades include: higher max loan (Rs. 7.5M vs Rs. 5M), interest-free microloans added, all agriculture sectors included, and 100% online application.

Q: Can a woman apply for the Kamyab Jawan / PMYB&ALS loan? Absolutely. 25% of total loan disbursements are strictly reserved for women entrepreneurs. Women receive priority processing and the same subsidized markup rates as male applicants.

Q: Can I take two loans simultaneously under PMYB&ALS? Yes , one short-term working capital loan and one long-term investment loan simultaneously, provided the combined amount does not exceed Rs. 7,500,000 total.

Q: What markup rate applies on Tier 1 Kamyab Jawan loans? The borrower pays a fixed 6% per annum on Tier 1 loans (Rs. 100,000–Rs. 500,000). The government subsidizes the full difference between 6% and the prevailing KIBOR+500bps rate , meaning the government pays the bulk of your interest for you.

Q: Do I need collateral for a Kamyab Jawan / PMYB&ALS loan? No collateral is required for Tier 1. For Tier 2 and Tier 3, a vehicle financed under the scheme may serve as collateral. Existing businesses applying for any tier require zero equity contribution.

Q: How can I get a free business plan for my PMYB&ALS application? Contact SMEDA at 111-111-456 , free business feasibility templates are available for all sectors. SMEDA has helpdesks in Lahore, Karachi, Peshawar, and Quetta with dedicated PMYB&ALS advisory support.

Final Thoughts

The PM Kamyab Jawan Loan 2026 , now PMYB&ALS , is Pakistan’s most powerful tool for turning youthful ambition into real economic impact. With Rs. 219 billion already placed in the hands of 287,541 young Pakistanis, the scheme is proven, active, and accessible today. Whether you want to start a poultry farm in Multan, build a tech startup in Lahore, open a restaurant in Karachi, or grow a dairy farm in Faisalabad , Tier 1’s 6% markup, zero collateral, and completely online process means the only barrier left is your own hesitation.

Apply today. Your business can start tomorrow.

Official Links:

- Apply Now: pmyp.gov.pk/bankform/newapplicantform

- Scheme Portal: pmybals.pmyp.gov.pk

- Loan Calculator: pmyp.gov.pk/pmyphome/Calculator

- SMEDA Free Advisory: 111-111-456

- Digital Youth Hub App: Available on Android & iOS