The PM Youth Business Loan Scheme 2026 , officially the PM Youth Business and Agriculture Loan Scheme (PMYB&ALS) , is Pakistan’s most impactful youth entrepreneurship initiative, offering loans from Rs. 100,000 to Rs. 7,500,000 at subsidized rates of 0% to 5% annually through 15 partner banks including HBL, Bank Alfalah, UBL, Bank of Punjab, and Sindh Bank.

Launched under PM Shehbaz Sharif’s Digital Youth Hub vision, the scheme has already disbursed Rs. 219 billion to over 287,541 beneficiaries across Pakistan. With no physical application form required and the entire process done at pmyp.gov.pk, this is the fastest government financing program available to young Pakistanis today. This complete 2026 guide covers every tier, every document, step-by-step online application, and 2026 updates you cannot miss.

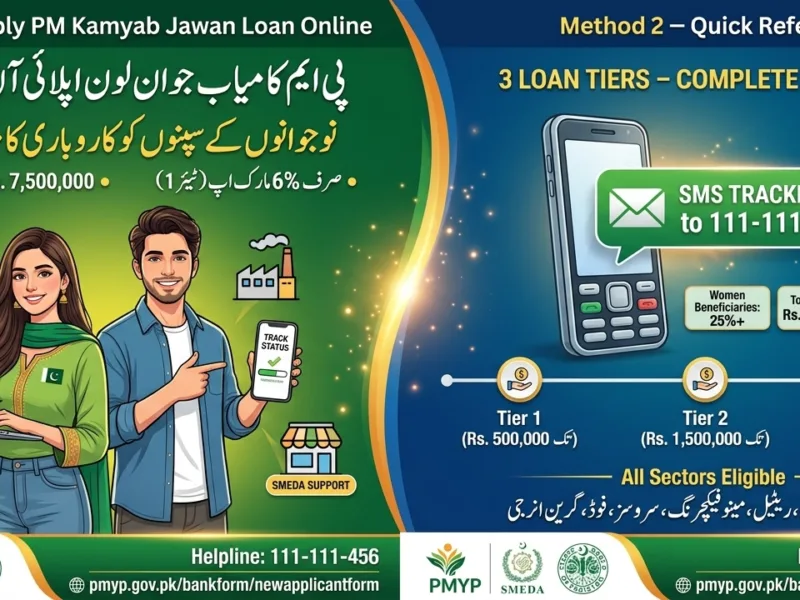

PM Youth Business Loan Scheme 2026 – Quick Reference

| Detail | Information |

| Official Full Name | PM Youth Business & Agriculture Loan Scheme (PMYB&ALS) |

| Official Portal | pmybals.pmyp.gov.pk |

| Apply Online | pmyp.gov.pk/bankform/newapplicantform |

| PMYP App | Digital Youth Hub (Android & iOS) |

| Total Partner Banks | 15 Commercial, Islamic & SME Banks |

| Loan Range | Rs. 100,000 – Rs. 7,500,000 |

| Interest on Tier 1 | 0% (Completely Interest-Free) |

| Age Limit | 21–45 years (18+ for IT/e-commerce) |

| Women’s Quota | 25% reserved for women entrepreneurs |

| Total Disbursed (2026) | Rs. 219 Billion to 287,541+ recipients |

| Helpline | 111-111-456 (24/7, toll-free) |

| SMEDA Support | Free business plan help at 111-111-456 |

| Regulatory Oversight | State Bank of Pakistan (SBP) |

3 Loan Tiers – Full Breakdown (Tier 1, 2 & 3)

The scheme is designed in three distinct tiers to serve every level , from first-time small business owners to serious entrepreneurs scaling to Rs. 7.5 million. The scheme offers three tiers, each supporting different business levels.

| Feature | Tier 1 | Tier 2 | Tier 3 |

| Loan Amount | Up to Rs. 500,000 | Rs. 500,000 – Rs. 1,500,000 | Rs. 1,500,000 – Rs. 7,500,000 |

| Markup Rate | 0% (Interest-Free) | ~5%–7% subsidized | Market rate subsidized |

| Repayment Period | Up to 3 years | Up to 5 years | Up to 8 years |

| Grace Period | Up to 6 months (optional) | Up to 1 year | Up to 1 year |

| Equity for New Business | 10% | 10% | 20% |

| Equity for Existing Business | Nil (Zero) | Nil (Zero) | Nil (Zero) |

| Collateral Required | Usually None | Minimal | Vehicle/asset as collateral |

| Best For | Small shops, freelancers, tutors | Growing businesses, trades | Manufacturing, IT firms, farms |

| Civil Works Financing | Up to 65% | Up to 65% | Up to 65% |

Important Clarification from HBL (Official): The loan under PMYB&ALS can be disbursed in tranches up to the amount approved by the bank and there is no restriction on the number of tranches that can be disbursed. There is no minimum amount of loan under Tier 1 and financing is allowed up to a maximum limit of PKR 0.5 million as per business needs of the customer.

Who Is Eligible? – 2026 Eligibility Criteria

Pakistani citizens with valid CNIC, aged 21–45 (18+ for IT/e-commerce) with entrepreneurial potential are eligible. No minimum education is required, but relevant qualifications help. A 25% quota for women entrepreneurs applies; priority is given to green/digital projects in 2026 updates. The scheme is not for government employees or those under other similar schemes. Clean credit history is mandatory.

You ARE eligible if:

- ✅ Pakistani citizen with valid CNIC or SNIC

- ✅ Age: 21–45 years (general) | 18+ years for IT/e-commerce businesses

- ✅ You have a viable business idea or running business , all sectors qualify

- ✅ Clean e-CIB record , no defaults on any bank or financial institution

- ✅ Not a government employee , civil servants are not eligible

- ✅ Not enrolled in any other government loan scheme

- ✅ Existing businesses: Nil equity required for all tiers

- ✅ Women entrepreneurs: 25% reserved quota , fast-tracked processing

You are NOT eligible if:

- ❌ You are a government employee at any level

- ❌ You are a bank defaulter , e-CIB will flag your record

- ❌ You are a non-resident Pakistani , scheme is for resident Pakistanis only

- ❌ You are already enrolled in another federal/provincial loan scheme

- ❌ Your CNIC is expired or not registered with NADRA

Documents Required – Complete Checklist

Documents required include CNIC copies, passport photo, business feasibility report, NTN, electricity bill consumer ID, and references (2 non-relatives). Vehicle registration is applicable if relevant.

| Document | Required For | Details |

| CNIC (Front & Back) | All Tiers | Original scan , valid, not expired |

| Passport-Size Photo | All Tiers | Recent, clear background |

| Business Feasibility Report | All Tiers | 1–2 pages: idea, projected income, costs |

| NTN (National Tax Number) | Tier 2 & 3 | Apply free at FBR.gov.pk if not registered |

| Proof of Residence | All Tiers | Utility bill or rent agreement |

| Bank Statement (6 months) | Tier 2 & 3 | Shows financial activity |

| Educational Degrees / Diplomas | Optional | Improves approval chances |

| Experience Certificates | Optional | Strengthens business credibility |

| References (2 non-relatives) | Tier 2 & 3 | Names, CNICs, and contact numbers |

| Vehicle Registration | If applicable | Required if vehicle is collateral |

2026 Update: January 2026 enhancements include mobile-friendly forms, reduced docs for verified accounts, women quota emphasis, and SMEDA templates for green/IT ventures.

How to Apply Online – Step-by-Step (Application Form Guide)

No physical application form is required. All applications have to be submitted online at pmyp.gov.pk/bankform/newapplicantform. Here is the complete process:

Step 1 – Create Your Account

- Visit pmybals.pmyp.gov.pk or pmyp.gov.pk

- Click “Apply Now” or “New Applicant Form”

- Register using your 13-digit CNIC and mobile number

- Verify OTP sent to your registered SIM

Step 2 – Fill the Application Form

- Enter personal details: name, address, date of birth, occupation

- Select your loan tier (Tier 1, 2, or 3)

- Choose your preferred partner bank from the dropdown (HBL, Bank Alfalah, UBL, BOP, Sindh Bank, etc.)

- Select your business sector (retail, agriculture, IT, manufacturing, services)

- Enter your business plan details , expected turnover, employees, monthly revenue

Step 3 – Upload Documents

- Upload all documents listed above , allow 15+ minutes for this step

- Ensure every upload is clear, readable, and in JPG or PDF format

- Blurry or cropped documents are the #1 reason for rejection

Step 4 – Submit & Track

- Click “Submit Application” and note your tracking ID

- Track status at pmybals.pmyp.gov.pk or SMS your tracking ID to 111-111-456

- Keep your mobile phone ON and audible , the bank will call for verification

Step 5 – Bank Verification & Disbursement

- After submission, your chosen bank reviews and verifies the application

- If approved, the bank contacts you for final document signing

- The loan amount is disbursed directly to your registered bank account within 7 to 10 working days after final approval confirmation.

Sectors Eligible for PM Youth Loan in 2026

All sectors and products are eligible. In the case of agriculture, all crop and non-crop sectors including crop production, livestock, poultry, fishery, and dairy are also eligible.

| Sector | Examples | Special Notes |

| Retail & Trade | Shops, wholesale, trading | All business scales |

| Agriculture | Crops, livestock, poultry, fishery, dairy | All crop and non-crop sectors |

| IT & E-Commerce | Freelancing, apps, online stores, SaaS | Age limit 18+; Matric required |

| Manufacturing | Small factories, food processing, garments | Up to 65% civil works financing |

| Services | Salons, repair shops, tuition academies | Tier 1 ideal for service startups |

| Green Energy | Solar-powered businesses, clean tech | Priority in 2026 processing |

| Healthcare | Clinics, pharmacies, medical labs | Tier 2 and 3 suitable |

| Construction | Small contractors, building materials | Vehicle as collateral for T2/T3 |

15 Partner Banks – Where to Get Your Loan

Loans provided under PMYB&ALS are processed through 15 Commercial, Islamic and SME banks. Key partner banks include:

| Bank | Type | How to Select |

| HBL (Habib Bank) | Commercial | Select in online form dropdown |

| Bank Alfalah | Commercial | Select in online form dropdown |

| UBL (United Bank) | Commercial | Select in online form dropdown |

| Bank of Punjab (BOP) | Provincial | Select in online form dropdown |

| Sindh Bank | Provincial SME | Email: pmloans@sindhbank.com.pk |

| Bank Al Habib | Commercial | Online portal selection |

| Meezan Bank | Islamic | Sharia-compliant structure |

| Allied Bank (ABL) | Commercial | Select in portal dropdown |

| NRSP (MFI) | Microfinance | For rural/remote applicants |

| Akhuwat Foundation | Islamic MFI | Interest-free community lending |

All eligible persons can apply for the loan by visiting pmyp.gov.pk. Select your preferred bank in the dropdown under “Bank Name.” Upon receiving the application online, the bank representative will contact you for application processing.

2026 Scheme Statistics – Real Numbers

So far, about 3,371,000 people have applied across Pakistan. Out of these, 1,135,000 applications are still in process, while 293,000 have been approved, and 287,541 people have already received their loans , totaling approximately Rs. 219 billion distributed. Around 1,943,000 applications were rejected or canceled due to errors in the application process.

| Metric | Number |

| Total Applications Received | 3,371,000 |

| Applications In Process | 1,135,000 |

| Applications Approved | 293,000 |

| Loans Already Disbursed | 287,541 beneficiaries |

| Total Amount Distributed | Rs. 219 Billion |

| Applications Rejected/Cancelled | 1,943,000 |

Why are so many rejected? The top 3 reasons for rejection are: (1) e-CIB default record, (2) unclear or incomplete document uploads, (3) CNIC mismatch with NADRA data. Avoid all three by checking your credit history first, scanning clean documents, and confirming your CNIC details are accurate before submission.

Free SMEDA Support – Get a Business Plan at Zero Cost

Small and Medium Enterprises Development Authority (SMEDA) has been tasked by PM’s Youth Programme with an advisory and supporting role to provide free guidelines to applicants.

SMEDA provides free business feasibility templates , the #1 document applicants struggle with. Contact your nearest SMEDA helpdesk:

| Province | Location | Contact |

| Punjab (Lahore) | Aiwan-e-Iqbal Complex, Egerton Road | 042-111-111-456 |

| Sindh (Karachi) | Bahria Complex II, M.T. Khan Road | 021-111-111-456 |

| KPK (Peshawar) | State Life Building, The Mall | 091-111-111-456 |

| Balochistan (Quetta) | Chaman Housing Scheme, Airport Road | 081-2831623 |

PMYB&ALS vs Kamyab Jawan – Key Differences

PMYB&ALS is the revised and renamed version of the earlier Kamyab Jawan Youth Entrepreneurship Scheme (PMKJ-YES). While they share the same core goal of empowering Pakistani youth aged 21–45 with low-cost loans for startups, SMEs, and agriculture, PMYB&ALS streamlines processes with tiered structures and explicit agriculture focus.

| Feature | PMYB&ALS (2026) | Kamyab Jawan (Old) |

| Agriculture Sector | Fully integrated, all crop/non-crop | Limited coverage |

| Application Process | 100% online, no physical form | Partial online |

| Tiered Structure | 3 clear tiers with distinct limits | Less structured |

| Women’s Quota | 25% strictly reserved | Not formalized |

| 2026 Updates | Mobile forms, SMEDA templates, green energy | Not updated |

| Current Status | Active , Apply Now | Replaced by PMYB&ALS |

Frequently Asked Questions (FAQs)

Q: What is the PM Youth Business Loan Scheme 2026? It is the PM Youth Business and Agriculture Loan Scheme (PMYB&ALS) , a government initiative offering Rs. 100,000 to Rs. 7,500,000 in loans at 0%–5% subsidized markup to young Pakistani entrepreneurs aged 21–45 through 15 partner banks. Up to Rs. 5 lakh (Tier 1) is completely interest-free.

Q: How do I apply for the PM Youth Loan Scheme online? Visit pmyp.gov.pk/bankform/newapplicantform, create your account with CNIC, fill the digital form, select your bank, upload documents, and submit. No physical application form is required , all applications are submitted online only.

Q: Is the PM Youth Loan really interest-free? Yes , Tier 1 loans up to Rs. 500,000 carry 0% markup. Tiers 2 and 3 carry subsidized markup rates of 5%–7% , still far lower than the 20%–25% commercial bank rates.

Q: Can women apply for the PM Youth Loan Scheme? Yes. 25% of the total loan volume is strictly reserved for women entrepreneurs , female applicants receive priority processing and additional subsidy benefits.

Q: Is collateral required for the PM Youth Loan? Tier 1 usually does not require collateral. For Tiers 2 and 3, minimal collateral such as a vehicle may be required depending on bank policy and loan amount.

Q: Can a freelancer on Fiverr or Upwork apply? Yes. Special provisions exist for IT professionals to buy hardware and equipment. IT/e-commerce applicants can apply from age 18 with at least Matriculation qualification.

Q: How do I check my PM Youth Loan application status? Track your application at pmybals.pmyp.gov.pk or SMS your tracking ID to 111-111-456. Keep your phone active as the bank will call directly for verification or approval confirmation.

Q: What is the helpline for the PM Youth Loan Scheme? The official helpline is 111-111-456, available 24/7 nationwide for inquiries, application status checks, and SMEDA business plan support; the same number serves all four provinces.

Final Thoughts

The PM Youth Business Loan Scheme 2026 has already delivered Rs. 219 billion to over 287,500 Pakistanis , transforming job seekers into job creators across every province. With a completely free Tier 1 loan of up to Rs. 500,000, a straightforward digital application, SMEDA’s free business plan support, and 15 partner banks to choose from, there has never been a more accessible moment to launch your business in Pakistan. Apply today , your only competition is your own hesitation.

Official Portal: pmybals.pmyp.gov.pk Apply Form: pmyp.gov.pk/bankform/newapplicantform Helpline: 111-111-456 (24/7) SMEDA Punjab: 042-111-111-456 Loan Calculator: pmyp.gov.pk/pmyphome/Calculator PMYP App: Digital Youth Hub (Android & iOS)

Read More: 9th Class Date Sheet 2026 – All Punjab, KPK, Sindh & Balochistan Boards (Complete Schedule)